Student Debt Crisis 2016: New Graduates Owe A Record-Breaking Average $37,000 In Loans

College students graduating this month across the United States can expect to feel nostalgic, field questions about their futures, and owe a lot for the education they just received. Student financial aid expert Mark Kantrowitz recently calculated that student borrowers in the class of 2016 are set to have the highest level of debt yet, at $37,172, the Wall Street Journal reported this week. This is up from about $35,000 last year.

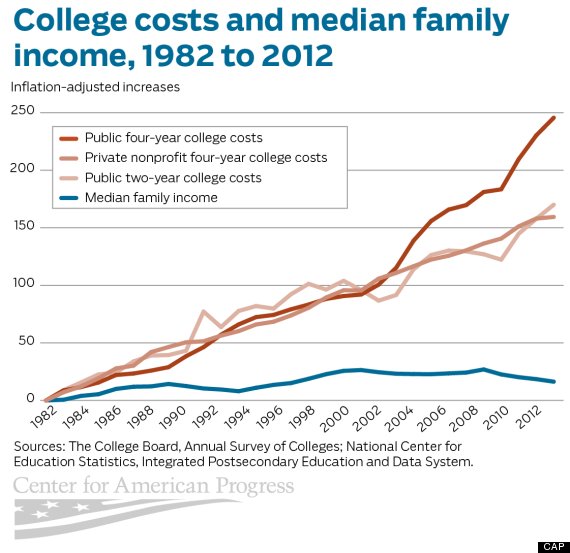

“It’s unfortunate that college costs are going up and the student aid, the grants, are not going up at the same rate on a per-student basis,” Kantrowitz, publisher and vice president of strategy at scholarship site Cappex, told the Journal last year. “College is becoming less and less affordable, though it’s still just as necessary.”

But if you’re getting ready to get your diploma, don’t despair. The White House announced in an April blog post the rates of recent graduates defaulting on their loan payments or becoming delinquent for not paying regularly have fallen in recent years. Meanwhile, CBS News noted the average starting salary for recent graduates recently has increased to $43,000, according to data released in January by the Federal Reserve Bank of New York.DYI Comments: The reason college costs are so high is due to student loans. The money didn't go to the student but straight to the University or College who saw this as nothing more than a cash cow allowing for continuous tuition increases. For every tuition increase all of the student loaning organization would increase the amount of loans, hence the vicious circle. Since bankruptcy is not allowed loaning organization including the Federal government(a tax) have a cash machine of interest income for years to come. Today ageing Boomers are having their Social Security garnished for unpaid student loans. Yes folks should pay their debts but once it gets to that point you are now trading one social problem for another.

There is a better way

To drop the costs for colleges, universities, technical training etc. is to allow for bankruptcy. Loans would be on the basis of the ability to pay as with any loan. This would immediately put a stop to the cash cow for the schools driving down the cost of schooling significantly. The administrators would scream to the heavens in an attempt to reverse this provision. If we have the political will (allowing bankruptcy) in about 5 years costs would (except for Ivy league) drop to where a student could work a part time job and 4 or 5 years later graduate debt free.

DYI

No comments:

Post a Comment