Whiff of Panic? Global Bear-Market Progress Report

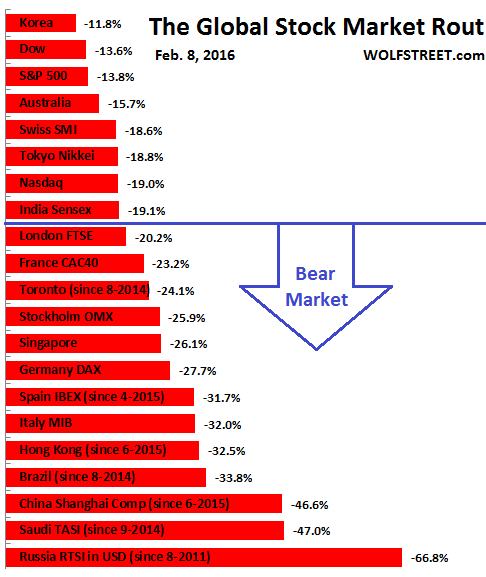

So here is the global bear market tracker. The Dow, though down 13.6%, is the second-best performer. A week ago, it was still the best performer. The Nasdaq, with its 5.4% loss last week and 2.8% so far today, has slipped further down the ladder and is approaching the bear market line, joining three other indexes in that neighborhood. Of the 18 non-US markets on the list, only five are not in a bear market (US markets as of this morning, European markets as of afternoon trading):

And folks are piling into government bonds. US Treasuries with longer maturities have been rising and yields have been falling, somewhat ironically, ever since the Fed raised rates in December. The 10-year Treasury yield is now at 1.75%, the lowest since almost exactly a year ago. These babes are hot!

Eurozone government bonds are even hotter, with the German 10-year yield at 0.22% today. Even fiscally challenged Italy gets to borrow 10-year money at 1.70%. But wait… these bonds have plunged today and yields have jumped 14 basis point from 1.56% on Friday. And Spain’s debt too has plunged today, with the 10-year yield jumping 11 basis points to 1.76%. It seems, investors are getting a little spooked about those two countries.

Alas, the 10-year yield of Japanese Government Bonds is teetering near zero, while any maturity below 10 years wallows in the Bank of Japan’s negative-yield absurdity.

So we still expect stock markets to rise this week, being firm believers in the principle that nothing goes to heck in a straight line. But as we said, that line could be straighter than we’d expect.

DYI Comment: My model portfolio remains steadfastly defensive despite the market selloff. Valuations are so elevated DYI's weighted formula has "kick us out" of stocks and bonds and rightfully so. Stocks and long term bond prices are so absurd historically Dollar cost averaging is NOT recommended. Alas this too will change. For the short term speculator The Great Wait would have been as long as eternity itself. For the historical/valuation player The Great Wait is nothing more than a blink of an eye.

In due time markets will become interesting(along with improved valuations).....I promise....Markets are regressing back to the mean and will overshoot as they always do. Our formula(it's no secret just click on the pages marked stocks, bonds, gold) will "kick us back in" as valuations improve and once they go beyond their mean will increase proportionally greater. Of course at that time uninformed folks will think you have lost your mind as you purchase bargains for the long haul. That is the life of a contrarian you're never be popular especially at the point of maximum pessimism or maximum optimism.

Updated Monthly

AGGRESSIVE PORTFOLIO - ACTIVE ALLOCATION - 2/1/16

[See Disclaimer]

Here’s my favorite Warren Buffett quote on this.

“A short quiz: If you plan to eat hamburgers throughout your life and are not a cattle producer, should you wish for higher or lower prices for beef? Likewise, if you are going to buy a car from time to time but are not an auto manufacturer, should you prefer higher or lower car prices? These questions, of course, answer themselves.

But now for the final exam: If you expect to be a net saver during the next five years, should you hope for a higher or lower stock market during that period?

Many investors get this one wrong. Even though they are going to be net buyers of stocks for many years to come, they are elated when stock prices rise and depressed when they fall. In effect, they rejoice because prices have risen for the “hamburgers” they will soon be buying.

This reaction makes no sense. Only those who will be sellers of equities in the near future should be happy at seeing stocks rise. Prospective purchasers should much prefer sinking prices.”

Simply, DYI's formula for stocks, Lt. bonds, gold(precious metals mining companies) answers the question "how much." When valuations improve your allocation is increased and when valuations decline so does your allocation. Since these three asset categories plus cash are so diametrically opposed there is a bull market somewhere.

DYI

No comments:

Post a Comment