Bubble

News

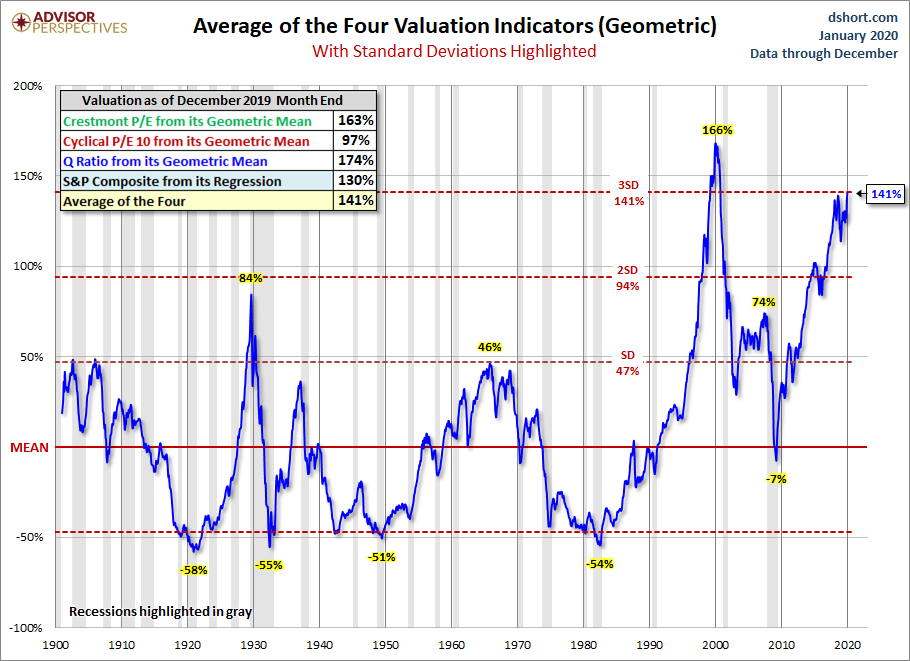

More likely, assuming that market valuations simply touch their run-of-the-mill historical norms in the future,

passive investors should be braced for zero or negative total returns both in the S&P 500 and in a conventional 60/30/10 asset mix over the coming 10-12 year horizon.

John Hussman

Whatever They’re Doing, It’s Not “Investment”

At the market open of Friday, January 24, our estimate of likely 12-year nominal total returns for a conventional passive investment portfolio (60% S&P 500, 30% Treasury bonds, 10% Treasury bills) fell to just 0.04% annually, below even the previous record of 0.34% set in August 1929. This extreme reflects the combination of record equity market valuations and depressed interest rates. That’s not an “equilibrium” situation. It’s a combination that joins insult with injury, creating weak prospects for the future returns of passive, diversified buy-and-hold strategies, across the board.

Understand this. The more glorious this bubble becomes in hindsight, the more dismal future investment returns become in foresight. The higher the price investors pay for a set of future cash flows, the lower the return they will enjoy over time. Whatever they’re doing, it’s not “investment.”

Amidst an “everything bubble” that has touched every asset class, I don’t believe that investors should imagine that there is some broadly appropriate investment that promises a satisfactory return despite such broad extremes. Even international stocks tend to lose significant value when U.S. stocks decline, regardless of their valuations. Yes, there may be niches that could be useful for diversification, but the primary “alternative” that investors have here, in my view, is cash, patience, and hedged investment exposure.

Thanks John

DYI