U.S.

Stock Market

Runs Out of Alpha!

Alpha is a risk-adjusted measure of "excess return" on an investment. It is a common measure of

assessing an active manager's performance or market index as it is the return in excess of "risk-free T-bills."

March 20, 2017

John P. Hussman, Ph.D.

Last week, Treasury bill yields rose to 0.75% following the Federal Reserve’s quarter-point hike in the target Federal Funds rate, placing the yield on even risk-free liquidity above our 0.6% estimate for 12-year prospective S&P 500 annual total returns. This isn’t the first time in history that prospective 12-year stock market returns have fallen below the prevailing T-bill yield, but it’s certainly the lowest return that has prevailed at any of those points.

Presently, based on the most historically-reliable valuation measures we identify, we expect annual total returns for the S&P 500 averaging just 0.6% over the coming 12-year period; a prospective return that we expect will not only underperform bonds over this horizon, but even the lowly yields available on risk-free T-bills.

Like the unwindings that followed the 2000 peak and the 2007 peak, there will be points in the interim where the prospective total return on stocks will likely be elevated (as a result of steep market losses and improved valuations), providing patient, flexible investors substantial opportunities for long-term total returns.

DYI: DYI has been “pounding the podium” that stock

returns will be sub atomically low – so much so – despite the absurd ultra low

interest rates driven by a mad cap world wide central banks including our own

Federal Reserve (it’s a private bank and they have no reserves) driving down

yields on bonds; stocks are now so elevated they are slanted to UNDERPERFORM 90

day T-bills!

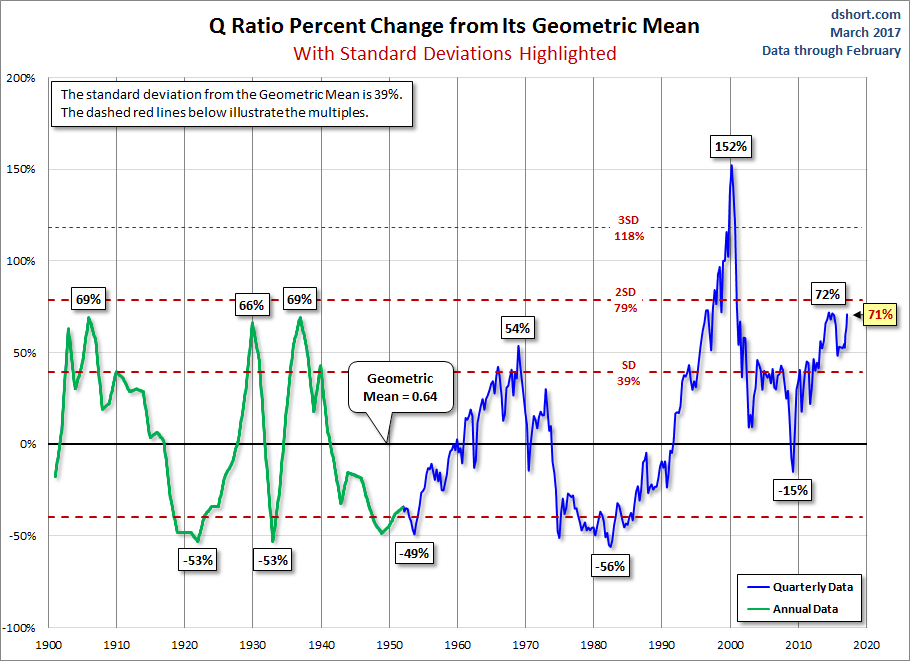

Stock

valuations are now so elevated in relation to sales, earnings, and DYI’s

favorite dividends; I moved my sentiment indicator, on March 12, 2017 back to

Max-Optimism forming a double secular top!

Market Sentiment

Smart Money buys aggressively!

Capitulation

Despondency

Max-Pessimism *Market Bottoms* Short Term Bonds

Depression MMF

Hope

Relief *Market returns to Mean* Gold

Smart Money buys the Dips!

Optimism

Media Attention

Enthusiasm

Smart Money - Sells the Rallies!

Thrill

Greed

Delusional

Max-Optimism *Market Tops* Long Term Bonds & U.S. Stocks

Denial of Problem

Anxiety

Fear

Desperation

Smart Money Buys Aggressively!

Capitulation

If

the Fed’s continue to increase interest rates DYI’s sentiment indicator for

long term bonds will move down from Max-Optimism to Denial of Problem improving

future returns. This will increase our

holdings of long term bonds computed by my weighted averaging formula.

Simply

put DYI is increasing into assets as their valuations improve and reducing

assets as their valuations decline.

Sounds easy – actually it is difficult for most individuals as it “moves

against the grain!” The great movements

in the market are caused by the MAJORITY of investor/speculators who by their

very nature are performance chasers – similar to dogs chasing cars – and despondent

sellers. Value players are dependent upon

the majorities – they’re in great abundance (thank goodness) – in order to

profit handsomely over the long haul.

What’s

the catch? I’ll give you a real life

example - me. In 1997 I began to exit stocks

aggressively due to valuation moving to the moon and yet from that time on, until

the top of the market, the NASDAQ went on to double again! What was I doing with the proceeds from the

sale of stocks? Buying gold and most

importantly precious metals mining companies as their valuations were on the

give – away – table! Out of step with

the majority of investor/speculators – YOU BET!

The mining companies didn’t begin their meteoric price rise until

2002! For little more than 5 years non

value players thought I was simply throwing away good money into a bad situation

and yet that time lag was a blessing allowing for addition savings into this beleaguered

asset category.

That

is the life of a long term secular historical value player who will experience

being “out of step” with the great majorities.

This is why this blog will never have a huge following as we know the majorities

are performance chasers and despondent sellers thereby it is mathematically

impossible. Those who do follow are in an

elite class of true long term historical value players who are the minority yet will earn the majority of the profits.

DYI