Recession???

Treasuries spread:

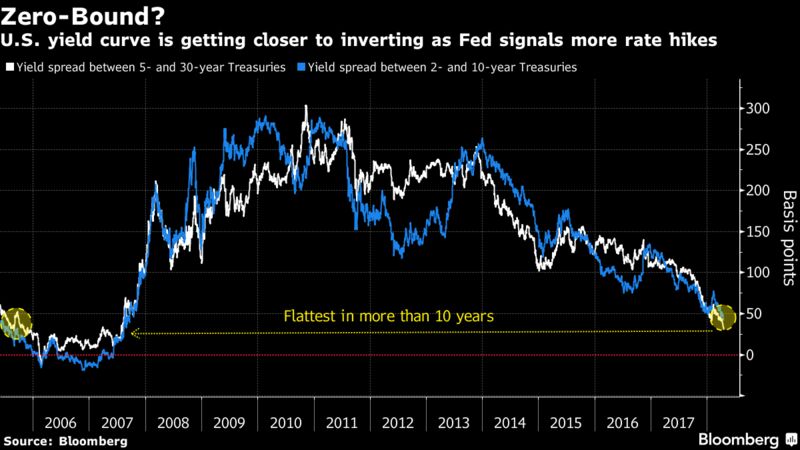

5 to 30 years hits narrowest since 2007!

Investors Are Getting Worried About an Inverted Yield Curve

The yield curve from 5 to 30 years flattened Wednesday to as little as 29 basis points, the narrowest spread since 2007. From 2 to 10 years, the gap touched 41 basis points, also the smallest in more than a decade. For extending to 10 years from 7, investors pick up a mere 4.3 basis points, less than a quarter of what they got a year ago.

If the barrage of Fedspeak this week is any indication, the persistent flattening is creating a dilemma for officials, who appear intent on gradually tightening policy. St. Louis Fed President James Bullard was the latest to weigh in, saying that central bankers need to debate the yield curve right now, and that it could invert within six months.

The Impact of an Inverted Yield Curve

As concerns of an impending recession increase,

investors tend to buy long Treasury bonds based on the premise that they offer a safe harbor from falling equities markets, provide preservation of capital and have potential for appreciation in value as interest rates decline.

As a result of the rotation to long maturities, yields can fall below short-term rates, forming an inverted yield curve. Since 1956, equities have peaked six times after the start of an inversion, and the economy has fallen into recession within seven to 24 months.

DYI: There

are four components that are strongly associated with U.S. economic downturns

[recessions].

- Widening credit spreads...NO

- Moderate, flat, or inverted yield curve...YES

- Falling stock prices...NO

- Purchasing Managers Index below 50...NO

Widening credit spreads between 5 year

T-Notes and Vanguard High-Yield Corporate Fund Investor Shares. 5 year T-Notes are currently yielding 2.80%

as compared to Vanguard’s High-Yield Fund at 5.41%. So far there hasn’t been much of a change for

Vanguard’s High-Yield Fund. When

investors begin noticing a slow down with the possibility of recession they

back off purchasing high yield paper thus prices fall and yields rise. So far been unable to check this indicator; for

an upcoming recession.

Yield curve no doubt about it the curve has definitely

flattened out. Once inversion occurs

most likely the economy will already be in recession making it prediction

ability of only stating the obvious.

Falling stock prices from 6 months earlier so

far despite stock price turbulence prices remain 4% higher. This indicator all by itself is of little

value as stock prices are well known for their volatility, however, when part

of the broader picture especially when stocks drop greater than 10% AND the remaining three indicators are negative a

high probability of recession is imminent.

Current Purchaser’s Managers Index report as

of March of 2018 is 59.3% definitely out from recession range however not

indicating an overheated economy as well.

The Fed’s desire to lift rates will continue but it will be muted to 25

basis points increases and possibly not at every meeting.

Conclusion:

So far recession is not in the cards however

since the yield curve has flattened DYI will be on the outlook monitoring my

other 3 indicators for any negative changes.

DYI

No comments:

Post a Comment